SK Hynix’s ADR lists on Nasdaq on July 10 — and here in Korea, the debate around it has been surprisingly heated. Some Korean shareholders and governance activists are openly criticizing the deal.

If you’re a foreign investor watching SKHY, you’ve probably seen some of these criticisms. Most of them sound reasonable at first — and most of them fall apart once you understand Korean tax law and regulations.

I live in Seoul and work in Korean finance. Let me walk you through the three biggest myths.

Myth #1: “They cancelled treasury shares, then issued new ones — that’s contradictory”

The criticism: SK Hynix held about 5.5% of its own shares as treasury stock. Instead of listing those existing shares as ADRs, the company cancelled them — and is now issuing new shares for the ADR. Critics call this dilution disguised as shareholder returns.

The truth: it’s about taxes.

Under Korean tax law, when a company sells treasury shares, the gain is taxed as corporate income. SK Hynix bought its treasury shares years ago at a fraction of today’s price — the stock is up several hundred percent since. Listing those old shares as ADRs would have been treated as a “disposal” and triggered a massive corporate tax bill.

Cancelling the treasury shares (a permanent reduction in share count — genuinely shareholder-friendly) and issuing a small amount of new stock instead was the tax-efficient path. The alternative would have burned billions of won in taxes — real shareholder value destruction.

Myth #2: “The ADR float is too small — TSMC listed 20% of its shares”

The criticism: SK Hynix’s new issuance is expected to be only around 2.5% of total shares. TSMC’s ADR float is over 20% of its shares, which is why it’s in every major U.S. index and ETF. A tiny float means no liquidity and no index inclusion.

The truth: two things critics miss.

First, SK Hynix legally cannot issue much more. Under Korea’s Fair Trade Act, its parent company SK Square must maintain at least a 20% stake. SK Square currently holds just 20.5% — barely above the line. A large new issuance would dilute SK Square below 20% and violate the law. The regulatory ceiling on new issuance works out to roughly 18–20 trillion won. This isn’t a choice; it’s a legal constraint.

Second, the TSMC comparison actually supports SK Hynix. TSMC’s 1997 ADR debut was also tiny — around 2% of shares, mostly stock that early investor Philips wanted to sell. TSMC’s ADR float grew to 20%+ over decades, as existing shareholders gradually converted their Taiwan-listed shares into ADRs.

Myth #3: “A small float means SKHY will stay illiquid forever”

The truth: the float will grow on its own.

Here’s the mechanism most commentary misses: once the ADR program exists, existing shareholders can convert their Korean shares into ADRs. Foreign investors hold roughly half of SK Hynix — many of them global funds that would prefer holding a dollar-denominated Nasdaq listing over Korean shares.

Just like TSMC, expect the ADR share of SK Hynix’s total float to rise steadily over the years. The July 10 listing is the starting point, not the final size.

My take from Seoul

Two things I’m watching as a Korean investor:

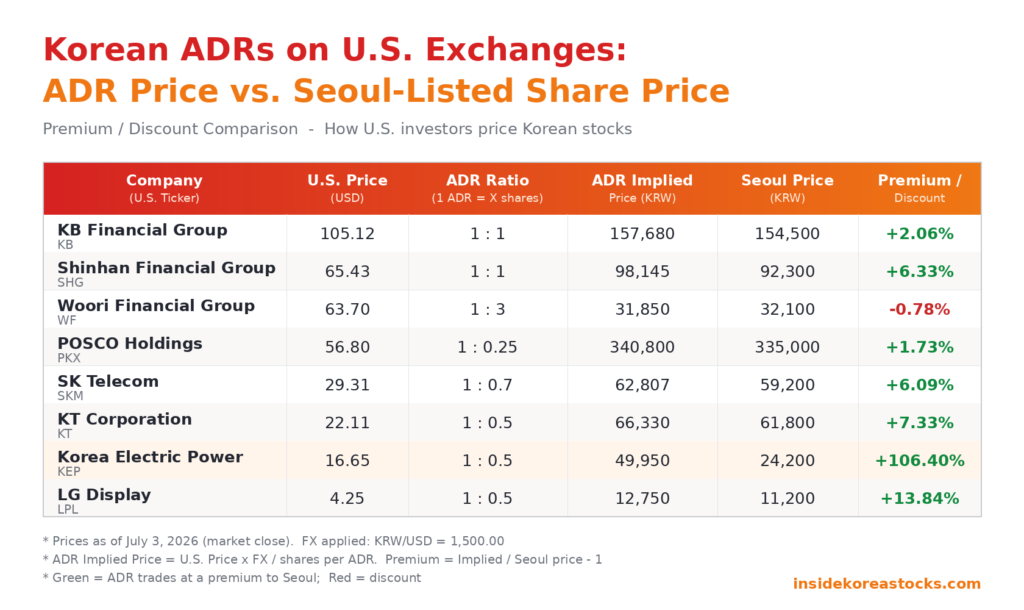

The price gap. Korean companies already listed as ADRs in the U.S. often trade at meaningful premiums to their Seoul-listed shares — in some cases the gap has run into double digits, and for one utility name it has exceeded 100%. Where SKHY settles relative to the Seoul listing will tell us a lot about how much of the “Korea Discount” is really just access friction.

Who leads whom. Korean academic research on existing ADR pairs found something interesting: price discovery tends to flow from the U.S.-listed ADR to the Korean shares, not the other way around. If that holds for SKHY, U.S. trading hours could start driving one of Korea’s most important stocks. That’s a structural shift worth watching.

The controversy in Korea is loud, but most of it evaporates when you look at the tax code and the holding-company rules. Management played the hand the regulations dealt them — and played it reasonably well.

I’ll be watching the July 10 debut closely from Seoul. Updates to follow.

Disclaimer: This is not investment advice. Always do your own research before investing.

insidekoreastocks.com — Real insights from someone actually living and investing in Korea.